It’s about knowledge - Research Cooperation

Research projects for the cooperation involve mathematical modeling for the financial markets with state of the art methods, machine learning techniques and data-driven implementation. The focus is to provide solutions for quantitative finance problems.

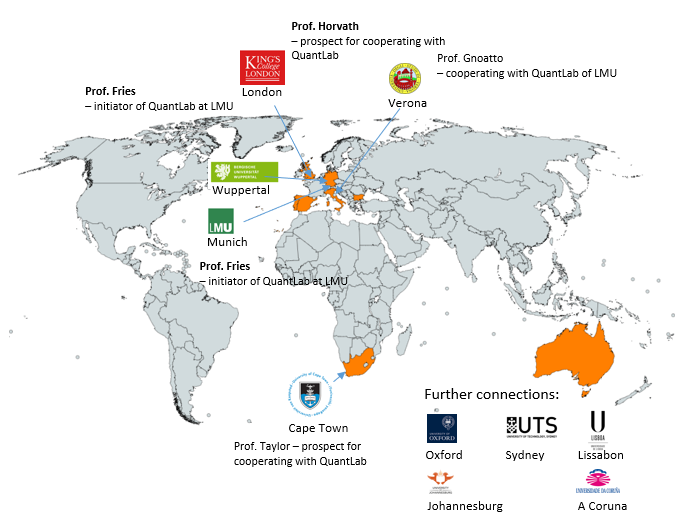

- Academia - strong relations to academic cooperation partners include:

- Ludwig Maximillian University Munich (Prof. Fries – QuantLab for Financial Math)

- University of Verona (Prof. Gnoatto – Financial Math)

- University of Cape Town (Prof. Taylor, Prof. McWalter – Financial Math)

- Kings College London (Prof. Horvath – Financial Math)

- University of Wuppertal (Prof. Ehrhardt / Prof. Günther, Computational Finance)

- Topics

- Option Pricing, Calibration and Hedging

- Machine Learning and its applications in Finance

- Proxies and Structures (Time Series, Smiles, Yield Curves, ...)

- Numerical Methods (ODE/PDE, Simulation, Transforms, ...)

- Accelerating and extending current methods

- Model Validation and Systemic Risk

- Conferences – personal contact to organizers include:

- WBS (Quant Conference, Machine Learning Conferences, MLI)

- KNect (Quant Minds, Risk Minds Europe/North America/Asia/Africa)

- PyData (The Python and Tech event)

- RISK (AI Conference)

- MathFinance

- ICCF - International Conference on Computational Finance

- Demonstrate strong relevance and skillset of the cooperation partners of BUW